「来週の決算説明会で海外投資家からの質問に対応しなければならないが、英語での回答に自信がない」

そんな状況で焦っているIR担当者は少なくないはずです。

2025年4月から東証プライム市場上場企業に対して、決算情報(決算短信・四半期決算短信・決算補足説明資料)および適時開示情報の英文同時開示が義務化されました。

なお、全文の英訳が必須というわけではなく、一部または概要の開示も認められています。

また、体制整備に時間を要する企業には、事前申請により最大1年間の猶予措置も設けられています(JPX資料によると約7%の企業が利用)。

この義務化に伴い、英文IR資料を読んだ海外投資家からの問い合わせや決算説明会への参加が増加しています。

書面での開示対応に加え、口頭での質疑応答に対応できる英語力の必要性も高まっているのが現状です。

本記事では、決算説明会Q&Aで頻出する質問20パターンと英語での回答例を提供します。回答例の[ ]部分に自社の数値を入れるだけで、そのまま想定問答集として活用できます。

Contents

- 1 1. 質問・回答例20選(カテゴリ別)

- 1.1 A. 業績ドライバー(1〜6)

- 1.1.1 Q1:Revenue growth drivers(売上成長の要因)

- 1.1.2 Q2:Gross margin change (mix/price/cost)(粗利率変動の要因)

- 1.1.3 Q3:Operating profit variance vs plan(営業利益の計画差異)

- 1.1.4 Q4:Segment performance: winners/losers(セグメント別業績)

- 1.1.5 Q5:One-off items / exceptional gains/losses(特別損益項目)

- 1.1.6 Q6:Working capital / inventory (cash conversion)(運転資本・在庫)

- 1.2 B. 見通し・ガイダンス(7〜11)

- 1.3 C. 戦略・競争・投資(12〜16)

- 1.3.1 Q12:Pricing power & competitive landscape(価格決定力と競争環境)

- 1.3.2 Q13:Market share / positioning(市場シェア・ポジショニング)

- 1.3.3 Q14:New products / roadmap (what you can disclose)(新製品・ロードマップ)

- 1.3.4 Q15:M&A strategy / acquisition criteria(M&A戦略・買収基準)

- 1.3.5 Q16:Cost reduction / efficiency program (quantify)(コスト削減・効率化施策)

- 1.4 D. 株主還元・資本政策(17〜19)

- 1.5 E. リスク・ESG・ガバナンス(20)

- 1.1 A. 業績ドライバー(1〜6)

- 2 3. コピペで使える「置換パーツ」集

- 3 4. 日本語をIRで伝わる英語にする最短ルール

- 4 5. 想定問答集に落とし込む手順

- 5 FAQ

- 6 まとめ

- 7 IR担当者向け英語講座のご紹介

1. 質問・回答例20選(カテゴリ別)

ここからは、決算説明会で実際に投資家から寄せられる質問を5つのカテゴリに分類し、それぞれに対する模範回答を紹介します。各回答は[ ]内に自社の数値を入れることで、そのまま使用できる形式になっています。

A. 業績ドライバー(1〜6)

Q1:Revenue growth drivers(売上成長の要因)

Q:

Could you walk us through the key drivers of your revenue growth this quarter?

What they mean(意図): 投資家は単なる売上成長率ではなく、その背後にある要因を理解したいと考えています。成長が一過性のものか持続可能なものかを判断し、今後の予測モデルに反映させることが目的です。

A:

Our revenue grew [X]% year-over-year to [¥Y billion]. The main drivers were threefold: First, volume expansion in [region/segment], which contributed approximately [Z]% of the growth. Second, price increases averaging [W]% across our portfolio. Third, favorable mix shift toward [higher-margin products]. On a like-for-like basis, excluding FX and M&A, organic growth was [V]%.

Point(注意・言い換え): 「threefold」「twofold」などを使って構造化すると聞き手が整理しやすくなります。為替影響がある場合は「on a constant currency basis」で補足し、比較可能性を確保しましょう。

Q2:Gross margin change (mix/price/cost)(粗利率変動の要因)

Q:

Your gross margin improved by 200 basis points. Can you break down the drivers of this improvement?

What they mean(意図): 粗利率の変動要因を「価格」「コスト」「構成比」に分解して説明してほしいという要望です。それぞれが持続可能かどうかを評価するための材料を求めています。

A:

Gross margin expanded from [X]% to [Y]%, an improvement of [200] basis points. This was driven by three factors: pricing contributed approximately [80] basis points as we implemented selective price increases in [Q2]. Cost reductions, primarily in raw material procurement, added another [70] basis points. The remaining [50] basis points came from mix improvement as sales of our [premium product line] increased as a percentage of total revenue.

Point(注意・言い換え): 「basis points(bp)」は利率や利益率の変動を表す際の標準的な単位で、1 basis point = 0.01%です。したがって100 basis points = 1%ポイントとなります。要因を定量化することで、投資家は自身のモデルを更新できます。

Q3:Operating profit variance vs plan(営業利益の計画差異)

Q:

Operating profit came in above your initial guidance. What drove the outperformance?

What they mean(意図): 計画を上回った要因が持続可能なものか、一時的な追い風によるものかを判断したいという意図があります。

A:

Operating profit exceeded our initial guidance by [¥X billion], or [Y]%. Approximately [60]% of this outperformance was structural, driven by better-than-expected cost efficiency and favorable product mix. The remaining [40]% was attributable to timing factors, including [delayed SG&A spending] and [one-time gains from asset sales]. We expect the structural improvements to continue into the next fiscal year.

Point(注意・言い換え): 「structural」と「timing factors / one-off」を明確に区別することで、投資家の懸念(「来期は反動減が来るのでは?」)を先回りして解消できます。

Q4:Segment performance: winners/losers(セグメント別業績)

Q:

Can you discuss which segments outperformed and which underperformed versus your expectations?

What they mean(意図): 事業ポートフォリオ全体ではなく、セグメント単位での強弱を把握し、今後のリソース配分や成長性を評価したいという意図です。

A:

In terms of segment performance, [Segment A] was the standout performer, with revenue up [25]% and operating margin expanding to [18]%. This was driven by [specific factor]. On the other hand, [Segment B] fell short of expectations, with revenue declining [5]% due to [specific challenge]. We are addressing this through [specific initiative], and we expect improvement in [timeline].

Point(注意・言い換え): 弱いセグメントについては、課題を認めた上で対策を述べることで、経営陣が状況を把握しコントロールしているという印象を与えます。

Q5:One-off items / exceptional gains/losses(特別損益項目)

Q:

There were some exceptional items this quarter. Could you quantify them and explain their nature?

What they mean(意図): 投資家は「正常収益力(normalized earnings)」を算出するために、一時的な損益項目を除外したいと考えています。

A:

This quarter included [¥X billion] in exceptional items. On the positive side, we recorded [¥Y billion] from the sale of [non-core asset], which was a one-time gain. On the negative side, we incurred [¥Z billion] in restructuring charges related to [specific program]. Excluding these items, our underlying operating profit was [¥W billion], representing [V]% growth year-over-year.

Point(注意・言い換え): 「underlying」「normalized」「adjusted」といった表現を使い、一時的要因を除いた実力ベースの数値を示すことが重要です。

Q6:Working capital / inventory (cash conversion)(運転資本・在庫)

Q:

Your inventory levels increased significantly. What is driving this, and how should we think about cash conversion going forward?

What they mean(意図): 在庫増加がキャッシュフローに与える影響と、それが戦略的なものか非効率によるものかを確認したいという意図です。

A:

Inventory increased by [¥X billion] quarter-over-quarter. This was a deliberate decision to secure supply of [critical components] ahead of anticipated demand in [Q4]. We expect inventory to normalize by [Q1 next fiscal year], with cash conversion cycle returning to approximately [Y days]. Our target remains to maintain working capital at [Z]% of revenue on an annual basis.

Point(注意・言い換え): 在庫増加が意図的なものであることを明示し、正常化のタイムラインを示すことで、投資家の懸念を払拭できます。「cash conversion cycle(CCC)」は、在庫購入から売上代金回収までの期間を日数で示す運転資本効率の標準指標です。

B. 見通し・ガイダンス(7〜11)

Q7:Full-year guidance rationale(通期ガイダンスの根拠)

Q:

Could you elaborate on the assumptions behind your full-year guidance?

What they mean(意図): ガイダンスがどのような前提条件に基づいているかを理解し、自身の予測との乖離要因を分析したいという意図です。

A:

Our full-year guidance is based on several key assumptions. First, we assume [no significant change in the macro environment / demand recovery in H2]. Second, we expect foreign exchange rates to remain around [¥X/USD]. Third, raw material costs are projected to [stabilize / decline slightly] from current levels. Under these assumptions, we project full-year revenue of [¥Y billion] to [¥Z billion], with operating profit of [¥W billion] to [¥V billion].

Point(注意・言い換え): 前提条件を明示することで、投資家は「もし為替が○○に動いたら」といったシナリオ分析を行うことができます。「conservative assumptions」という表現を使うと、慎重な姿勢をアピールできます。

Q8:Sensitivity: FX / commodity / rates(感応度分析)

Q:

What is your sensitivity to foreign exchange movements, particularly USD/JPY?

What they mean(意図): 為替やコモディティ価格の変動が業績に与える影響を定量的に把握し、リスクシナリオを構築したいという意図です。

A:

Regarding FX sensitivity, a [¥1] movement in USD/JPY impacts our annual operating profit by approximately [¥X billion]. Our guidance assumes an average rate of [¥Y/USD] for the full year. For reference, our current hedge ratio is approximately [Z]% for the next [12 months]. Similarly, a [1]% change in [key raw material] prices would impact gross margin by approximately [W] basis points.

Point(注意・言い換え): 感応度は具体的な数値で示すことが重要です。ヘッジ状況も併せて説明することで、リスク管理能力をアピールできます。

Q9:Demand outlook & pipeline visibility(需要見通しと受注残)

Q:

How would you characterize demand visibility at this point, and what does your order pipeline look like?

What they mean(意図): 将来の売上の確度を評価するために、受注残や商談パイプラインの状況を把握したいという意図です。

A:

Our demand visibility remains [solid / challenging] depending on the segment. In [Segment A], we have approximately [X months] of backlog, which is [above / in line with] historical levels. In [Segment B], while orders remain soft, we are seeing [early signs of recovery / stabilization]. Our sales pipeline for large deals is [healthy], with [Y] qualified opportunities representing approximately [¥Z billion] in potential revenue over the next [12-18 months].

Point(注意・言い換え): 「visibility」は予測の確度・見通しの透明度を表す重要なIR用語です。定量的なバックログ情報を示すことで説得力が増します。

Q10:Capex plan & expected return(設備投資計画と期待リターン)

Q:

Can you walk us through your capital expenditure plans and the expected returns on these investments?

What they mean(意図): 設備投資が成長投資なのか維持更新投資なのか、またそのリターンを把握して資本効率を評価したいという意図です。

A:

Our capex plan for this fiscal year is [¥X billion], up [Y]% from last year. Of this, approximately [60]% is growth-related investment in [new production capacity / R&D facilities], with expected IRR of [Z]% and payback period of [W years]. The remaining [40]% is maintenance capex to sustain current operations. We remain disciplined in our capital allocation, with a hurdle rate of [V]% for growth investments.

Point(注意・言い換え): 投資を「growth capex」と「maintenance capex」に分類することで、成長への姿勢を示すことができます。IRR(Internal Rate of Return:内部収益率)は、投資から得られるキャッシュフローの正味現在価値をゼロにする割引率を指し、投資案件の収益性評価に広く使用される指標です。ハードルレートは投資判断の最低基準となる期待収益率を示します。

Q11:Medium-term targets progress (ROE/ROIC etc.)(中期目標の進捗)

Q:

How are you tracking against your medium-term targets, particularly ROE and ROIC?

What they mean(意図): 中期経営計画で掲げた資本効率目標に対する進捗を確認し、経営陣のコミットメント度合いを評価したいという意図です。

A:

We are making [solid / steady] progress toward our medium-term targets. ROE improved to [X]% this fiscal year from [Y]% in the base year, and we remain on track to achieve our [Z]% target by [FY20XX]. ROIC similarly improved to [W]%, reflecting both margin expansion and disciplined capital allocation. The key initiatives driving this include [specific measures]. We provide a detailed update on medium-term progress in our [annual report / IR presentation], which is available on our website.

Point(注意・言い換え): 目標に対して順調であれば「on track」、やや遅れている場合は「making progress but below our initial expectations」といった表現を使い、正直に現状を伝えましょう。

C. 戦略・競争・投資(12〜16)

Q12:Pricing power & competitive landscape(価格決定力と競争環境)

Q:

How would you assess your pricing power in the current competitive environment?

What they mean(意図): インフレ環境やコスト上昇を価格に転嫁できる力があるかどうか、競争優位性の持続性を評価したいという意図です。

A:

We believe we have [strong / moderate] pricing power, particularly in [specific segment / product line] where we hold [market position] and offer [differentiated value proposition]. This fiscal year, we successfully implemented price increases averaging [X]% with minimal impact on volume. That said, we remain mindful of competitive dynamics and prioritize value over pure price increases. Our strategy is to [maintain / strengthen] pricing through [product innovation / service differentiation] rather than cost-based competition.

Point(注意・言い換え): 「pricing power」は収益性の持続可能性を示す重要な概念です。競合の動向に言及しつつも、自社の強みを強調しましょう。

Q:

Has your market share changed, and how do you view your competitive positioning?

What they mean(意図): 市場での相対的な地位がどう変化しているかを把握し、成長の持続性を評価したいという意図です。

A:

Based on [industry data / our estimates], our market share in [key market] is approximately [X]%, which represents [an increase of Y percentage points / stable performance] compared to last year. We attribute this to [specific factors]. Our positioning as [market leader / challenger / niche player] allows us to [benefit from scale / focus on high-value segments]. We expect to [maintain / grow] share through [strategic initiative].

Point(注意・言い換え): 第三者データがある場合はその出典を明示し、自社推計の場合は「our estimates」と断りを入れましょう。

Q14:New products / roadmap (what you can disclose)(新製品・ロードマップ)

Q:

Can you give us any color on your product roadmap for the next 12-18 months?

What they mean(意図): 成長ドライバーとなる新製品・サービスの投入予定を把握し、将来の収益貢献を予測したいという意図です。

A:

While I am limited in what I can disclose due to competitive sensitivity, I can share that we have [X] significant product launches planned for [FY20XX]. These include [general description without specifics]. We expect these new products to contribute approximately [Y]% to revenue growth in [timeline]. For more detail, please refer to our [Technology Day / Product Showcase] scheduled for [date].

Point(注意・言い換え): 競争上の理由で詳細を開示できない場合は、その旨を明確に伝えた上で、開示可能な範囲の情報を提供しましょう。

Q15:M&A strategy / acquisition criteria(M&A戦略・買収基準)

Q:

How are you thinking about M&A as part of your growth strategy, and what are your acquisition criteria?

What they mean(意図): オーガニック成長の補完としてのM&A姿勢を理解し、買収による希薄化リスクや統合リスクを評価したいという意図です。

A:

M&A is an important component of our growth strategy, but we remain highly selective. Our criteria include: strategic fit with our [core business / adjacency], financial discipline with a target IRR above [X]%, and cultural alignment for successful integration. Our current M&A pipeline is [active / building], though we have nothing to announce at this time. We maintain [¥Y billion / sufficient capacity] for opportunistic acquisitions while prioritizing organic growth.

Point(注意・言い換え): 具体的な案件については言及を避け、あくまで方針レベルでの回答にとどめましょう。「opportunistic」という表現は、焦ってM&Aを追求していないことを示します。

Q16:Cost reduction / efficiency program (quantify)(コスト削減・効率化施策)

Q:

Can you provide more detail on your cost reduction initiatives and quantify the expected savings?

What they mean(意図): コスト削減施策の進捗と効果を定量的に把握し、マージン改善の持続性を評価したいという意図です。

A:

Our cost efficiency program, launched in [FY20XX], targets cumulative savings of [¥X billion] by [FY20YY]. To date, we have achieved [¥Y billion], or [Z]% of the target. Key initiatives include [procurement optimization], which contributed [¥W billion], and [operational efficiency / headcount optimization], which contributed [¥V billion]. We expect to achieve the full target by [timeline], with approximately [U]% of savings reinvested in growth initiatives.

Point(注意・言い換え): 削減目標、進捗、具体的な施策、再投資計画をセットで説明することで、単なるコストカットではなく戦略的な効率化であることを示せます。

D. 株主還元・資本政策(17〜19)

Q17:Dividend policy / payout ratio(配当方針・配当性向)

Q:

Can you explain your dividend policy and how you think about the payout ratio going forward?

What they mean(意図): 株主還元に対する経営陣のコミットメントを確認し、インカムリターンの予測可能性を評価したいという意図です。

A:

Our dividend policy targets a payout ratio of [X]% to [Y]% of consolidated net income on a stable and sustainable basis. For this fiscal year, we plan to pay an annual dividend of [¥Z per share], representing a payout ratio of [W]%. We have maintained or increased dividends for [V consecutive years], and our policy is to [progressively increase dividends / maintain stable dividends] while balancing growth investment needs.

Point(注意・言い換え): 「stable and sustainable」という表現で、安定性と持続可能性を強調しましょう。増配実績がある場合はアピールポイントになります。

Q:

How are you thinking about share buybacks as part of shareholder returns?

What they mean(意図): 自社株買いに対する姿勢を確認し、資本効率改善へのコミットメントを評価したいという意図です。

A:

Share buybacks are an important tool in our capital return framework. We consider buybacks when [our stock is undervalued / we have excess cash beyond growth investment needs]. This fiscal year, we executed [¥X billion] in buybacks, representing approximately [Y]% of our market capitalization. We will continue to evaluate buyback opportunities based on [stock price valuation / cash position / growth investment requirements], with a flexible approach rather than a fixed target.

Point(注意・言い換え): 自社株買いの基準(株価水準、余剰現金など)を明示することで、規律ある資本配分姿勢を示せます。

Q19:Cash allocation (growth vs return)(キャッシュ配分の優先順位)

Q:

How should we think about your capital allocation going forward—growth investment versus shareholder returns?

What they mean(意図): 成長投資と株主還元のバランスをどう考えているかを把握し、中長期的な株主価値創造の方向性を理解したいという意図です。

A:

Our capital allocation framework prioritizes [disciplined growth investment] while ensuring [attractive shareholder returns]. Specifically, we allocate capital in the following order: first, [organic growth investment including R&D and capex]; second, [M&A opportunities that meet our strategic and financial criteria]; third, [shareholder returns through dividends and buybacks]. We target a [net cash / net debt] position of [¥X billion / X times EBITDA] to maintain financial flexibility. Shareholder returns will be considered within the range of maintaining a sound balance sheet.

Point(注意・言い換え): 優先順位を明確にすることで、投資家は経営陣の考え方を理解できます。「disciplined」という表現を使うことで、無謀な投資はしないという姿勢を示せます。

E. リスク・ESG・ガバナンス(20)

Q20:Key risks & mitigation (supply chain, geopolitics, regulation)(主要リスクと対応策)

Q:

What are the key risks to your business, and how are you mitigating them?

What they mean(意図): 事業リスクを経営陣がどの程度認識し、対策を講じているかを確認したいという意図です。リスク管理能力は経営品質の指標として重要視されています。

A:

We have identified several key risks and are actively managing them. First, [supply chain risk]: we have diversified our supplier base from [X] to [Y] suppliers and increased inventory buffers for critical components. Second, [geopolitical risk]: our exposure to [region] is approximately [Z]% of revenue, and we are [monitoring the situation closely / developing contingency plans]. Third, [regulatory risk]: we are proactively engaging with regulators regarding [specific regulation] and have allocated resources for compliance. While we cannot eliminate all risks, we believe we have appropriate mitigation measures in place.

Point(注意・言い換え): リスクを認めつつも、対策を講じていることを具体的に示すことが重要です。「We are managing this」という曖昧な表現ではなく、具体的な施策を述べましょう。

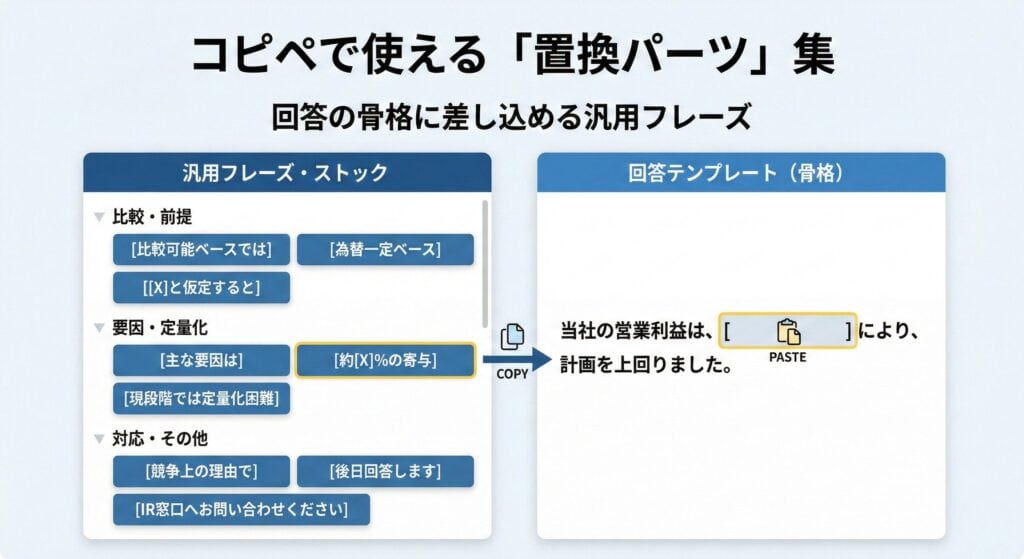

3. コピペで使える「置換パーツ」集

回答の骨格に差し込める汎用フレーズを整理します。

| 用途 | 英語表現 |

| 比較可能ベース | On a comparable / like-for-like basis, … |

| 為替一定ベース | On a constant currency basis, … |

| 主要因の提示 | The main driver was … |

| 定量化 | This contributed approximately [X]% / [¥Y billion] |

| 前提条件 | Assuming [X], we expect … |

| 保守的前提 | Based on conservative assumptions, … |

| 定量化困難 | At this stage, it is difficult to quantify … |

| 競争上の理由 | We do not disclose this as it is competitively sensitive. |

| 後日回答 | We will get back to you after we verify the data. |

| IR窓口誘導 | Please feel free to reach out to our IR team. |

4. 日本語をIRで伝わる英語にする最短ルール

日本語をそのまま英訳しても海外投資家には伝わりにくいことがあります。米国証券取引委員会(SEC)が1998年に発行した「A Plain English Handbook」で提唱された原則を参考に、効果的な表現方法を解説します。

受動態→能動態

| 避けるべき | 推奨 |

| It is expected that revenue will grow. | We expect revenue to grow. |

| Consideration is being given to … | We are considering … |

能動態を使うことで、誰が主体で何をするのかが明確になります。

確度に応じた動詞選択

「Maybe」「Probably」の多用は曖昧さを印象付けます。

| 確度 | 表現 |

| 高い(80%以上) | We expect / We are confident |

| 中程度(50-80%) | We estimate / We anticipate |

| 低い(50%未満) | We assume / We project (under certain assumptions) |

冗長表現の削除

| 冗長 | 簡潔 |

| In order to achieve | To achieve |

| Due to the fact that | Because |

| At this point in time | Now / Currently |

結論ファースト

避けるべき: 市場環境が厳しい中、様々な取り組みを行いましたが、売上は前年比5%減でした。

推奨: Revenue declined 5% year-over-year, primarily due to challenging market conditions, despite our initiatives.

5. 想定問答集に落とし込む手順

Step1:10問を選ぶ

20問すべてが毎回聞かれるわけではありません。以下の観点から優先度の高い10問を選定します。

選定基準:今期の業績変動が大きい項目、前回深掘りされた論点、アナリストレポートで言及されたテーマ、競合決算で注目された論点、新たに発表した施策(M&A、組織変更等)。

Step2:各回答に3要素を入れる

選んだ質問に対して、以下の3要素を必ず含めます。

定量データ(KPI):売上成長率、利益率、市場シェアなど。要因2つ:シンプルに構造化(多すぎると印象に残らない)。次の打ち手:「今後どうするか」で経営の方向性を示す。

Step3:答えられない領域を確定

競争上の理由や未公表情報など、回答できない質問への対応を事前に決めます。

なぜ開示できないか(理由)、代わりに何を伝えられるか(範囲)、いつ追加情報を提供するか(フォロー)の3点を準備します。

Step4:社内レビュー

想定問答集は複数部門のレビューを経て完成させます。

経理:数値の正確性。法務:開示規制への準拠、インサイダー情報該当性。経営企画:戦略との整合性。IR:前回説明会との整合性。

FAQ

Q. 決算説明会で多い英語の質問は?

大きく5カテゴリに分類されます。最も多いのは「業績ドライバー」(売上成長要因、利益率変動)で、次いで「ガイダンス」(前提条件、感応度)、「戦略・競争」(価格決定力、M&A)、「株主還元」(配当、自社株買い)、「リスク」(サプライチェーン、地政学)が続きます。

Q. 答えられない質問への対応は?

「We cannot disclose this as it is competitively sensitive. What I can tell you is [開示可能範囲]. We will provide more detail when [タイミング].」の3ステップで対応します。単に「No comment」で終わらせないことが信頼構築につながります。

Q. ガイダンスの前提を伝える表現は?

「Our guidance is based on the following assumptions: …」で前提を提示し、「Under these conditions, we expect revenue in the range of … to …」でレンジを示し、「Key sensitivities include …」で感応度を伝えます。

Q. Plain Englishとは?

SEC(米国証券取引委員会)が1998年に「A Plain English Handbook」で提唱した、投資家にわかりやすい英語表現の原則です。能動態の使用、冗長表現の削除、結論ファーストの構成などが基本となります。

まとめ

決算説明会での英語Q&Aは、海外投資家との信頼関係を構築する重要な機会です。本記事の20の質問・回答例を活用し、[ ]に自社数値を入れた想定問答集を準備してください。

重要なのは流暢さではなく、質問の意図を捉えた論理的な回答です。

事前準備を徹底することで、どんな質問にも自信を持って対応できるようになります。

IR担当者向け英語講座のご紹介

海外投資家との対話において、最も避けるべきは準備不足による不適切な対応です。質問の意図を理解できなかったり、不正確な情報を伝えてしまったりすることは、企業への信頼を損なう可能性があります。

一方で、適切な準備と訓練によって、明確で誠実な回答ができれば、それが投資家との信頼関係構築の基盤となります。

本番でうまく答えられなかったら…そんな不安が少しでもある方へ

海外投資家との1on1やインタビューでは、事前に想定されるQ&Aを準備していたとしても、その場で英語で伝える力が問われます。

とはいえ、IR業務で忙しい中、英語の準備に多くの時間は割けない。

そんな現場の声に応えるために作られたのが、「IR担当者向け英語講座」です。

✅ 自社IR資料を教材にする実践演習

✅ 実際の海外投資家がよく使う表現や質問パターンを網羅

✅ ネイティブ講師と1on1形式でのトレーニングも可能